Farms & Factories: European VC's Divergent Decade

European startups received €159 billion of funding over the past decade. Yet, an increasingly select group of stakeholders drive most of the topline figures.

"Well, farmers never have made money. I don't believe we can do much about it."

Said US President Calvin Coolidge in the 1920s, opposing subsidies to a buoyant agricultural industry in surplus since the Great War, but now facing resurgent global competition. The subsequent 1929 Wall Street Crash then contributed factors leading to the Dust Bowl, both promptly decimated the agriculture industry.

What exactly does this have to do with an article about startups in Europe 100 years later? The example highlights the need to maintain industry ecosystem balance: when an area is succeeding, the temptation of complacency is a butterfly effect risk.

Over the past decade, trends in European startups and venture capital have led to more emphasis on later-stage investing, more concentrated in number, but greater in size. These factories supply significant output gains, fed by the ecosystem of farms (startups) that grow into them. In recent years, early-stage investing has lagged later-stage on growth, the ramifications of which may cause bottlenecks and "supply shortages" going into the 2020s.

The Case for Europe

Startups and investors in Europe have been beating their chests for several years now. With the world's third-largest population (446 million) and second-largest GDP ($15.6 trillion), a range of characteristics help the European Union stick out as a place to create companies and invest in:

- Open borders for business and migration

- 1.1 million STEM graduates per year (2017) and 6 million professional developers

- Stagnant wage growth and employment opportunities for the unlucky Millennial generation

- Clustered centres of speciality in areas such as finance, design, and biotech

Despite stakeholder efforts and the strong-looking optics, there are regular partisan cries of European venture being half-baked. Sifting through the arguments and data—with inevitable comparisons to the US—my conclusion is that European VC is succeeding, albeit in a distorted manner:

- Rising capital allocations to later-stage investing

- Seed and early-stage investing plateaued around 2015

- Suboptimal exit liquidity, masked by the skew of big wins

- Fundraising AUM increasingly going to proven veterans, despite growing first-time fundraising numbers

With the help of industry and broader macroeconomic data, I will demonstrate why this is happening and some potential remedies.

Europe has the factories, but let's not forget about its farms.

Startup Investment: 2015 Plateau

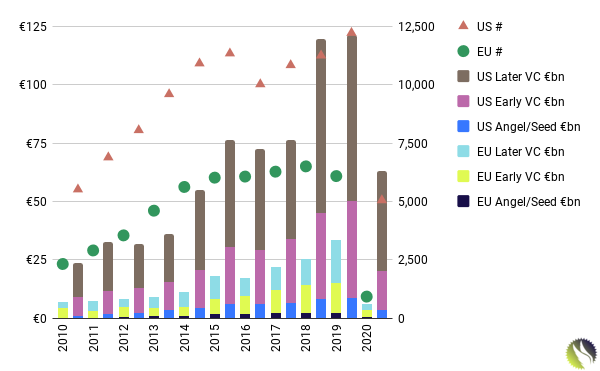

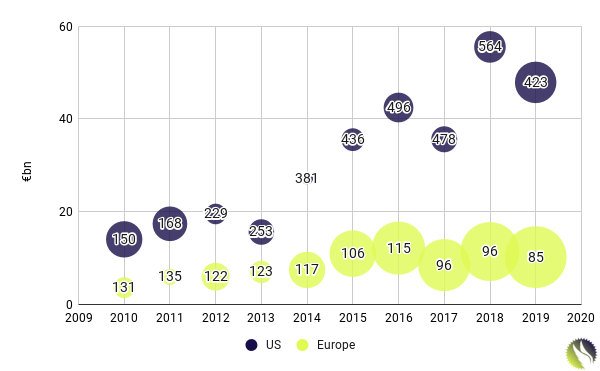

European startups garnered €159 billion of investment over the past decade (Pitchbook), reaching €34 billion in 2019 alone. Despite paling in both largesse and growth to the US equivalent of €645 billion, Europe's trajectory of funding and numbers grew in unison at around 41% CAGR. In contrast, in the States, number growth (37.4%) lagged the amount figures (44.3%).

Total Startup Financing: USA and Europe, 2010 - Q1 2020

The disparity between American growth of amounts and numbers gives credence to the growing disconnect of "haves and have-nots," whereby fewer companies are taking more of the pie.

Despite its top-level parity, digging further into European data paints a similarly disjointed picture. While 2019 European funding amounts were 4.7x higher than in 2010, the respective numbers multiple was lower at 2.6x. The number of European startups funded per year has also remained stagnant in the 6,000s since 2015. Are there push or pull factors: is 6,000 a natural capacity, or is investment focus rationalising into a smaller subset of companies?

So, Europe is experiencing similar conditions to the US: more funding to fewer companies, albeit occurring over the past five years, instead of the entire decade.

Round Types

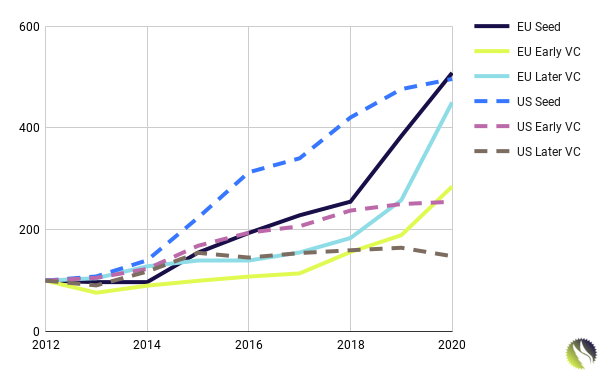

Pitchbook data shows that later-stage investing is outperforming in Europe. Its share of total funding has grown from 37% to 56% over the decade; being the only stage to have exceeded the US equivalent in funding growth. Exuberance is evident in median round sizes, on an indexed basis, European later-stage rounds have grown at a pace traditionally seen in Seed.

A key point of observation is the lack of growth in US later-stage round medians. Such figures suggest that the advent of mega-rounds has not permeated into all levels of this stage.

Median Startup Round Size (Indexed): USA and Europe, 2012 - Q1 2020

Somewhere, lost in the middle is European Early-Stage VC rounds, the subsector with the lowest growth across all the regional metrics. Its total amount CAGR at 36.2% is 7.2% lower than the US and represents the only marked divergence between the regions.

Seed investing shows a decline in numbers across both regions since 2014. But there is a fork in the road in terms of amounts raised. The US is showing fervour, with annual investment totals almost tripling over the decade, while Europe is a malaise of stagnant growth.

First-time Startup Financing: USA and Europe, 2010 - Q1 2020

In the States, even seed-stage companies are now in the bracket of haves and have nots, while Europe is becoming an even more exclusive club, albeit with parsimonious rewards on offer.

So, in a nutshell, we are seeing:

- US: more for less across the board

- Europe: a rush to later-stage and selective caution at earlier stages, which may have a bottleneck effect in future years.

Exits: Wilderness in the Middle

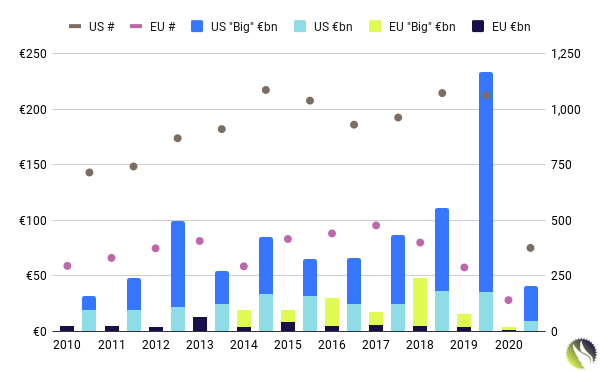

The early web 2.0 startup harvest brought bountiful exits across all regions over the 2010s. From 2014-2019 Europe realised €154 billion (Dealroom) of proceeds, compared to €689 billion (Pitchbook) in the US, both with relative parity of 50% CAGR. 2018 was one for Europe's ages, as a collective exhale released whales like Spotify and Adyen into public markets.

The narrative of Europe having weak exit markets is dispelled by the relative growth parity achieved with the US over the decade. However, the difference in amounts between the two is stark; total exits over the US's five years were 4.5x higher than Europe's €154 billion. For comparison, funding differences between the two were a closer 4.1x.

Under the hood, data suggests that Europe has a problem with exit flow and churning companies of all outcomes. Exit behaviours in Europe are a big game hunt: Large outcomes from a relatively smaller group of companies that generate significant returns.

Startup Exit and Big Exit Activity: US and Europe, 2010 - Q1 2020

"Big" exits in Europe (>€250 million) have remained stable at an average of 76% of all exit amounts over the five years. Yet, while exits and big exit amounts have grown at a similar pace (50% CAGR), big exit numbers grew significantly less than total (36% to 51%). This means that the inequality of exits is increasing: the "Gini coefficient" is widening, with fewer companies constituting more of the spoils. For comparison, in the States, numbers are more uniform, the only disconnect being that big exit (>$500 million) total amount growth (54.8%) shaded all exits by 4.7%.

Average exit size has shrunk over the years in Europe by 0.5% on a compounded basis. Each year the figure oscillates wildly, a sign that it's directed by big exits, which have risen by a healthy 10.6% over the period. US data is less disparate than Europe's, with total and big averages growing by 6.1% and 9.2%.

What this all means is that European outcomes are two extremes: big exit or insignificant return. While this true to form of the VC home run investing mantra, rising seas are lifting all the boats in the US. Big exits are up, but so is the average exit amount; middle-market M&A deals allow also-rans to exit respectably. A VC portfolio return won't be defined 3x'ers, but the ripple effects of this to founders, investors, and the like is important.

Europe presents a wilderness in the middle where startups and their investors are left with more illiquid exit options when it becomes clear that they are not a Spotify.

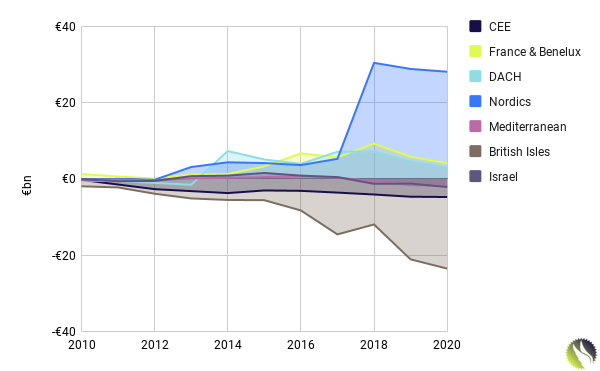

Regional

If we look at each region's "investment account" of net exit proceeds - fundraising for the period, it provides an excellent visual representation of how balanced activity is across the continent. Over the decade, DACH, France & Benelux and the Nordics were net up, with the latter winning big. Substantial investment has gone into the British Isles, which may either be a leading indicator towards an upcoming decade of exits, or over-confidence in UK startups.

VC Investment Account (Cumulative Exits - Investments): European Regions, 2010 - Q1 2020

Along with round trends, exit patterns suggest that the prominent VC gatekeeper role will remain strong: the best funds, get the best deals and the best exits. This pattern signalling starts early in a startup's life and directs its trajectory in a stark manner.

Fundraising: Newcomers and Well-resourced Veterans

The 2010s saw significant increases in capital commitments to venture capital funds around. This trend was driven by a range of macroeconomic factors (mass liquidity to all), to the subjective narrative build-up that tech will be driving stock market returns as sentiment pivoted from value to growth.

Over the decade, total venture capital raised in Europe grew by at a CAGR of 41.8% (Pitchbook), broadly the same as in the US. Yet, within these figures some familiar disparities emerge:

- 3,578 funds raised in the States, compared to Europe's 1,126

- Annually, the number of European funds raised has dropped over the decade.

- European median fund size grew by a CAGR of 19.4%, compared to 2.46% in the US.

- Annual amounts raised in the States were more volatile.

VC Fundraising, €bn (Y), Median (Z) and Number (Label): USA and Europe, 2010 - 2019

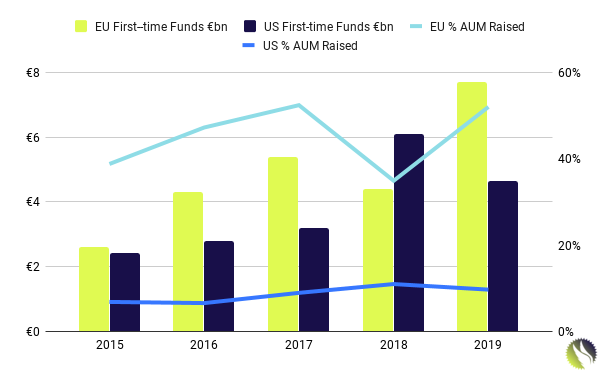

Where Europe is showing a positive trend is in supporting first-time fundraisers. According to Invest Europe, in the second half of the decade, first-time fundraises accounted for 45.6% of all new AUM, compared to 8.8% in the US (Pitchbook).

First-time VC Fundraising: USA and Europe, 2015 - 2019

Putting the two together comes up with another empty middle-ground situation:

- Increased overall AUM overall +

- Stagnant numbers of funds raised +

- Larger median fund size +

- Many first-time funds =

- Lots of new small funds and a cadre of well-resourced veterans.

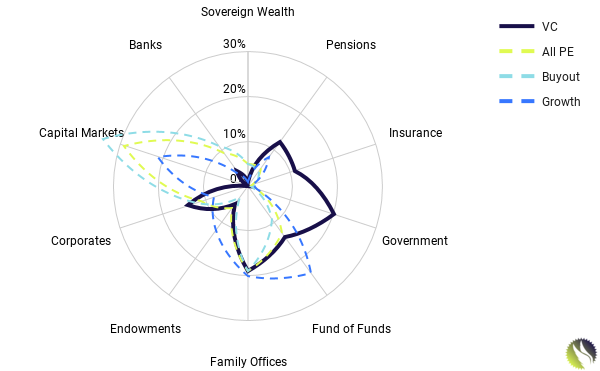

A look into Invest Europe's data about LP composition shows that VC LP bases are a tale of two halves. While on the one hand, there is strong support from governments (24% of all LP commitments 2014-2018), family offices and corporates (including CVC), but when it comes to more fluid institutional sources, European VCs remain overlooked. The bulk of buyout and growth equity capital comes from deeper-pocketed institutional capital markets.

Private Equity LP Composition: Europe, 2019 (578 funds, 392 firms)

It should be a priority in the 2020s for VCs to get more institutional capital. Fortunately, winds are in their favour.

On a collective level, Europe's pensions savings total €6.8 trillion (OECD, 2019). Equity crowdfunding has been a hit with retail investors, Mainland Europe and UK figures show that over €500m was invested in 2018 alone. Despite the platform having a proven playbook for driving viral b2c adoption, especially for Fintech, there is also an argument that crowdfunding is full of dregs that funds gave a pass on. There seems to be an appetite for the wider public to access VC exposure through financial assets. Will fund managers take notice?

Conservative investing attitudes limit appetite for venture capital, which is entirely rational when dealing with retail life savings. There are also issues related to finding track records in Europe longer than ten years. As per Thomas Kristensen of LGT Capital Partners:

You've got asset owners trying to invest into a relatively small portion of a universe of 600 managers ... Trying to find the ones that will be winners can be very tricky.

But when we see the number of first-time funds raised, there is evidence that LPs are making braver leaps.

Many investment trusts and OEICs that can be invested in pensions offer limited exposure to VC. In the UK, there are the Draper Esprit, Augmentum Fintech, and Merian Chrysalis investment trusts. Baillie Gifford has also been increasingly offering a broader range of private tech exposure through its stable. But where is the fund of funds vehicle that can give pension funds, investment managers, and savvy retail investors access to the European VC basket?

A fund of funds model would help spread risk and be a more cautious opening for pension savings. It exists for Private Equity, why not VC?

Country Performance: Policy and Culture

Looking at country-level performance can be a poisoned chalice in Europe. Without digressing into politics, Europe's core competitive advantage (free movement of trade and people) makes intra-border comparisons of VC funding tenuous and with potential red herrings.

Over 2014-19 according to Dealroom's data of €170.4 billion total European investment, over half (56%) was directed to the large markets of the UK, Germany, and France. What does this mean? It demonstrates a slightly lopsided capital allocation: the three countries constituent 41.6% of European GDP. More significantly, it's a reflection of the Western European magnet, which the EU's fluid system allows. Brain drain - especially in Eastern Europe - is a major societal issue, and a myriad of idiosyncrasies and policy choices limit movement the other direction, despite some reversal trends.

Total Startup Financing: European Countries, 2014 - Q1 2020

UiPath is a generational success story for Romania, but its growth included an HQ relocation to New York. Does it demonstrate that great companies form anywhere, but are they still "located" back home when they grow and attention shifts? Why does this matter? It's not merely down to patriotic reasons for ranking humble brags, it's for the spillover effects that an HQ offers: property prices, employment, skill-sharing, side hustles, and angel investing. Incidentally, out of the countries that raised over €1 billion, Romania, Switzerland, France, Sweden, and Norway experienced the fastest funding growth over 2014-19.

An excellent example of the power of staying put is bootstrapped mobile gaming giant Nordeus, which grew out of its original base in Belgrade, Serbia. Correlation or causation that Serbia has had one of the highest growth rates in fundraising since 2014 (119%)?

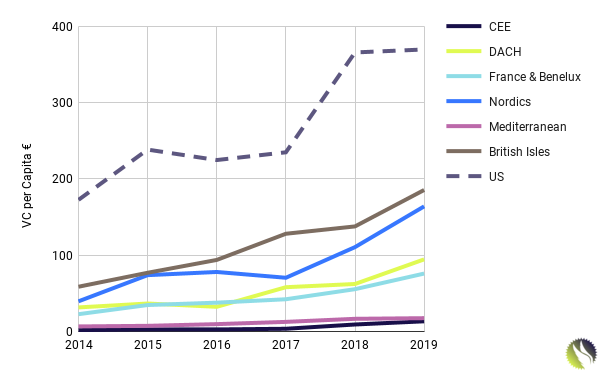

VC per Capita

A holistic way of demonstrating the strides that Europe needs to make, in terms of realising the potential of investing in startups is to look at VC per capita. Using the same logic as used for GDP (for country investment figures) shows how even the strongest European regions are way behind the US.

VC per Capita: USA and European Regions, 2013 - 2019

Overall, trends are growing and perhaps may tell a different story by the decade's end. There are some strong points within these figures: Sweden, Switzerland, Ireland, and the UK. At the other end of the scale, Italy's average numbers are spartan (€11), and Poland's (€6) belie its broader economic growth story.

What Limits Company Creation in Europe?

Money to invest and companies to invest in: a chicken and egg situation? There have been significant funds raised and spent by European funds, yet annually European VCs invest equivalent amounts into American and Canadian startups as they do at home. What has limited investable startup growth in Europe?

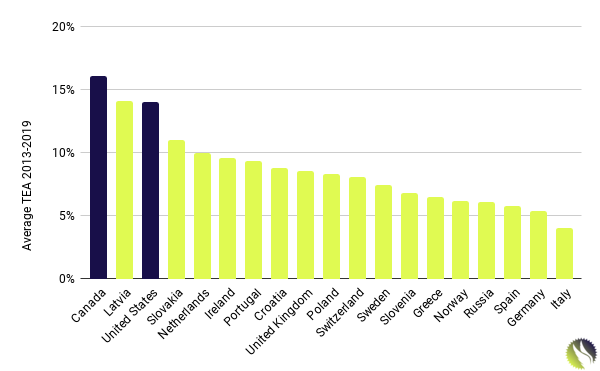

Global Entrepreneurship Monitor (GEM) measures indicators that contribute to early-stage startup activity, the most prominent being the percentage of adults that own/operate new ventures ("TEA"). The findings of the data shed light on what is holding Europe back.

Average Early-stage Entrepreneurial Activity (TEA) % of Adults: Europe, US and Canada 2013 - 2019

Bar Latvia, every country underperforms the US and Canada. The GEM data surveys 12 factors that contribute to the entrepreneurial vibrancy, which gives clues towards the underperformance of European TEA. The three most substantial areas of weakness for the continent to address are financing, taxes and bureaucracy, and cultural/social norms. Out of the 12 factors, Europe underperforms relative to the US in nine areas, most significantly in the following:

- Cultural and Societal Norms: -1.29

- Taxes and Bureaucracy: -0.54

- Financing for Entrepreneurs: -0.52

The three in which Europe outperforms shows Europe offers fairer markets and more involved/useful governments:

- Governmental Programs: 0.27

- Entry Regulation: Internal Market Dynamics: 0.18

- Entry Regulation: Internal Market Openness: 0.07

Addressing conservative cultural norms of not fearing failure and shunning the stable blue-chip career is the biggest hurdle for investible company creation in Europe. That finance is also an impediment may suggest that the two are not mutually exclusive.

Build a Balanced Ecosystem of Farms and Factories

Overall, Europe's VC and startup sectors are considerably healthier than they were a decade ago. Many may lament it not happening sooner. Perhaps if the 2000s weren't spent with the brightest minds devoting their time to packaging asset-backed securities, Europe now would be a powerhouse. But hindsight is a beautiful thing.

What is clear is that a bifurcation is emerging between the top of class and the rest. This splinter is more pronounced in Europe than in the US. The data presents a Pareto principle case that a minority of funds and companies have driven most growth in rounds, exits, and fundraising. On an overall level, this has dragged up the numbers to suggest growth, but it masks a degree of stagnancy, especially within early-stage markets, secondary countries, and contender funds.

Factories have been prioritised over farms and this will manifest in supply chain imbalances. In terms of what's to come and what should change, here are my thoughts.

1. An upcoming bottleneck of top-of-class startups

Appetite is very much towards the later-stage of investing and there is ample dry powder available. But the more benign growth and attention in early-stage markets hints that it will be very competitive to get into the next batch of blue-chip startups.

For proven funds, the seed investments they make will have real signalling power and further the overall dichotomy between haves and have nots.

2. More seed funds are required. Those that run new playbooks will succeed

With attention gazing towards the later-stage, those that focus on earlier stages will likely reap the rewards. Established funds in this space will have an immense opportunity due to imbalances of the past decade. New fund managers will have their chances, but likely will have to try something different to stand out. I think the days of a 20 startup seed roster will evolve. LPs will want more actionable output for their 2/20, and that could manifest in the next seed funds trying things like:

- Quasi consulting/creative studio business models with investing models: a coalescence of the "platform" and "studio" models into a revenue-generating business line and brand differentiator for the fund

- Entire sandbox plays, establishing investments across the continent with more localised scout networks or remote teams

- Use of technology to source and deploy capital more en-masse (across more startups) and more automated (fewer people and lower management fees)

3. Institutional fund commitments will rise due to the effects of Modern Monetary Theory, value-to-growth tilt, and retail demands

A widening of the VC LP base will bring more capital to the table and bring about behavioural shifts. If more institutional money arrives from pensions, banks, and capital markets, their more quantitative approaches will lead to fund governance shifts.

If more exposure is made available through OEICs and investment trusts to VC assets, private investors will increasingly access the asset class, leading to more attention and the same virtue-signalling evangelising that you see from the Monzo crowdfund and Tesla day-trader types.

4. Whale-type exits will continue to dominate unless middle-market M&A emerges.

While acqui-hires, write-offs, and zombie companies prevail everywhere, Europe has a problem with providing investors with an exit route for startups in the "respectable" range of multiples. The data shows that this segment has contributed to a more extensive and egalitarian set of exit figures in the US.

Conjecture abounds about the conservative nature of M&A in corporate Europe, but whether right or wrong, middle-market exit routes should increase. In the aftermath of COVID-19, corporate Europe could be in for an extended period of consolidation, which could hamper this. Private Equity and management buyout options could be another avenue. PE has increasingly participated in growth-stage transactions, and there may be further opportunities for middle-market funds to take controlling stakes in sustainable startups.

5. Smaller Countries with focused strategies continue to succeed. Eastern and Southern Europe need a break.

Throughout the analysis, certain countries always came up with favourable metrics: Estonia, Latvia, Iceland, and Ireland. Luxembourg and Malta also, but are difficult to parse due to their fiscal advantages. Smaller countries can concentrate resources and efforts better to build significant (relative) wins.

It's most likely that UK, France, and Germany will continue to dominate in absolute terms, and the Nordics will outperform in relative terms. What is not clear is how emergent regions of CEE and Southern Europe can increase their trajectory. Talent is not the issue; it seems more around capital, confidence, and ecosystem.

The opportunity that I see brightest for these regions is the post-Covid pivot to remote. How this plays out with wider investor nets, team formation, and cost efficiencies could manifest in more favourable conditions for building out ecosystems in the emergent hubs.